Obamacare has delivered another sucker punch to the middle class. This time it’s sticker shock.

Now that a few people can get past the tech problems of HealthCare.gov and actually see the real cost of insurance plans available, they are finding that Affordable Care is big hit to the family budget. And when the family budget gets hit in the solar plexus, guess what happens to consumer spending and the economy.

In California, policies for about 900,000 Californians are being canceled because of Obamacare’s mandates and about 2/3rd of these do not qualify for subsidies, according to The Chicago Tribune. The result—these folks will be paying higher premiums.

In Alabama, premiums have doubled for some middle class families like Courtney Long, a stay-at-home mother of four. She told WHNT News. “It’s devastating. I started crying,” said Long. “I mean, we have worked so hard to get out of credit card debt, get ahead on the car loan, transfer our mortgage to a 15 from a 30 year mortgage… and for what?”

In Tennessee, Sen. Lamar Alexander (R-TN) issued an analysis of a White House report and found the following:

— Today, a 27-year-old man in Memphis can buy a plan for as low as $41 a month. On the exchange, the lowest state average is $119 a month — a 190 percent increase.

— Today, a 27-year-old woman in Nashville can also buy a plan for as low as $58 a month. On the exchange, the lowest-priced plan in Nashville is $114 a month — a 97 percent increase. Even with a tax subsidy, that plan is $104 a month, almost twice what she could pay today.

— Today, women in Nashville can choose from 30 insurance plans that cost less than the administration says insurance plans on the exchange will cost, even with the new tax subsidy.

— In Nashville, 105 insurance plans offered today will not be available in the exchange.

In Washington State, Obamacare will increase the underlying cost of individually purchased health insurance by 34-80 percent on average, according to Forbes. The list goes on and on and includes Texas, Florida, New York, Illinois, Georgia and North Carolina. But premiums are just the beginning. The deductibles are outrageous, too.

A piece in Saturday’s The New York Times tells the story of Doug and Ginger Chapman, ages 55 and 54, a middle class couple “sitting on the health care cliff.” Their annual income of around $100,000 a year makes them ineligible for a subsidy in New Hampshire (if they earned under $94,000, it would cut their costs by half). They have to replace their family insurance which includes the two of them and their two sons. The premium cost alone, not including any deductible is $1,000 a month, or 12 percent of their income.

A piece in Saturday’s The New York Times tells the story of Doug and Ginger Chapman, ages 55 and 54, a middle class couple “sitting on the health care cliff.” Their annual income of around $100,000 a year makes them ineligible for a subsidy in New Hampshire (if they earned under $94,000, it would cut their costs by half). They have to replace their family insurance which includes the two of them and their two sons. The premium cost alone, not including any deductible is $1,000 a month, or 12 percent of their income.

The Times’ analysis found the following:

“The cost of premiums for people who just miss qualifying for subsidies rises rapidly for people in their 50s and 60s. In some places, prices can quickly approach 20 percent of a person’s income. Experts consider health insurance unaffordable once it exceeds 10 percent of annual income. By that measure, a 50-year-old making $50,000 a year, or just above the qualifying limit for assistance, would find the cheapest available plan to be unaffordable in more than 170 counties around the country, ranging from Anchorage to Jackson, Miss.”

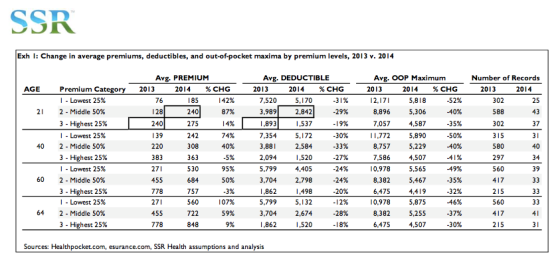

The other group that gets disproportionately hit is the young, according to Forbes. For a 40 year old, the 2013 average deductible was $4,045, and the cost increased 29 percent to $309. For a 64-year-old man, the cost of a plan with a $3,494 deductible increased 64 percent to $806.

The Real Impact of Obamacare is Yet to Come

If even a fraction of the middle class and upper middle income earners divert some of their discretionary dollars to pay for health care, it will have a significant impact on consumer spending. What will that mean for the economy? Consumer spending accounts for about 70 percent of the nation’s GDP, although experts say that number is likely to decline.

The top 20 percent of income earners account for about 40 percent of all spending in the U.S. When you increase the costs of health care and the new taxes associated with Obamacare, you can hear the wallets closing. LINK

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}